Car insurance, often viewed as a grudging expense by many, is actually a complex and invariably necessary part of modern driving. It’s not just a legal requirement in most jurisdictions but a critical financial safety net. The world of car insurance is dense with variables, each influencing the cost and coverage of policies. In this analysis, we’ll dive deep into the essentials of car insurance, unpacking everything from the basic necessities to how you can intelligently manage your insurance costs.

What to Know About Car Insurance

Learn about car insurance basics, how to determine the necessary coverage, factors influencing rates, obtaining quotes, available discounts, coverage options, claims process, and reviews. – Basics: Types of coverage and why it’s important. – Coverage Amount: Factors to consider when determining how much insurance is needed. – Rates & Quotes: Information on what affects rates and how to get a quote.

Car Insurance Basics

Car insurance is fundamentally about protection. It safeguards you, your finances, and others on the road in the event of an accident. Understanding its basics is akin to understanding why you wear a seatbelt its not just about following rules; its about safety and financial prudence.

From personal experience, the first car accident I was involved in was minor, but the ramifications without insurance could have been financially crippling. This incident taught me the critical value of comprehensive coverage. Statistics show that the average cost of an auto liability claim for property damage was $3,638 in 2020, and $18,417 for bodily injury. The numbers alone make a compelling case for robust coverage.

Every driver must know at least three types of basic car insurance: – Liability Insurance: Covers the costs if you are at fault in an accident and you damage someone else’s property or cause injuries. – Collision Insurance: Covers damage to your own car after an accident, regardless of who is at fault. – Comprehensive Insurance: Covers damage to your car caused by external factors like theft, vandalism, or natural disasters.

How Much Car Insurance Do I Need?

The amount of car insurance you need largely depends on your specific circumstances. When I purchased my first car, the dealer suggested the minimum liability coverage. However, after consulting with an insurance advisor, I realized that given my frequent long-distance travel, opting for more than the minimum was prudent.

Heres a brief guideline: – State Requirements: Start with the minimum required by your state. – Asset Protection: If you have significant assets, consider higher liability limits to protect against potential lawsuits. – Vehicle Value: If you drive a newer or higher-value vehicle, collision and comprehensive coverage are advisable.

Experts often recommend that if your assets are substantial, you should opt for liability limits of at least $100,000 per injury and $300,000 per accident. This is where personal umbrella policies come into play, providing additional coverage where your standard policy caps.

What Affects Car Insurance Rates?

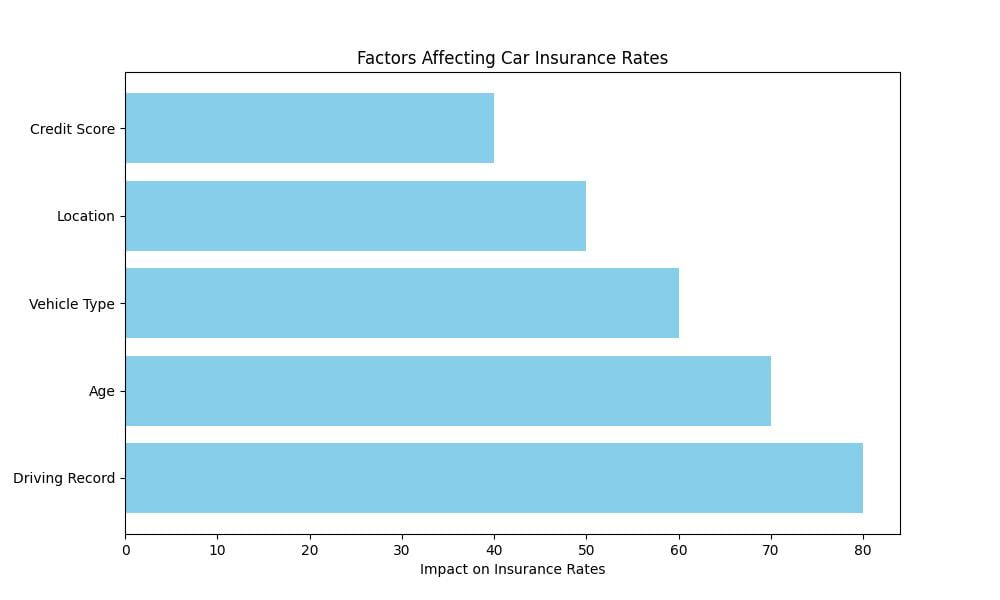

Several factors influence car insurance rates, which can vary dramatically from one person to another. Your age, driving history, and even credit score can play significant roles. Young drivers, for instance, might find their rates substantially higher due to the perceived risk associated with their inexperience.

For example, after moving to a metropolitan area, I noticed a spike in my premiums. It was explained that higher traffic density increases the likelihood of accidents, thus inflating rates. This is corroborated by research indicating that urban drivers pay up to 20% more than their rural counterparts.

Key factors include: – Driving Record: A clean driving record can lower premiums significantly. – Credit Score: Many insurers use credit scores to predict the risk of issuing a policy. – Age and Gender: Statistically, certain demographics pose more risk. – Location: Urban areas typically have higher rates than rural areas.

How to Get a Car Insurance Quote

Getting a car insurance quote is easier than ever thanks to online platforms. Typically, youll need to provide some basic information about yourself, your vehicle, and your driving history. I found that gathering all necessary documents beforehand significantly simplifies the process.

Heres a quick checklist for what youll likely need: – Personal Information: Including your drivers license and social security number. – Vehicle Information: Make, model, and year, plus the vehicle identification number (VIN). – Driving History: Details of any past accidents or violations.

Car Insurance Discounts

One of the more positive aspects of car insurance is the availability of discounts. Many companies offer a variety of ways to save, from safe driver discounts to reductions for eco-friendly vehicles. Personally, I benefited from a multi-policy discount when I bundled my car and home insurance, which trimmed my premiums by 15%.

Common discounts include: – Multi-policy Discount: Save when you bundle car insurance with other policies. – Safe Driver Discount: Available if you have a clean driving record. – Student Discounts: Often available for those with good academic records.

Car Insurance Coverage Options

Beyond the basic types, there are several other coverage options that can be tailored to fit individual needs. For instance, as someone who enjoys road trips, I find roadside assistance coverage indispensable.

Additional options to consider: – Uninsured Motorist Coverage: Protects you if youre hit by a driver without insurance. – Personal Injury Protection (PIP): Covers medical expenses and lost wages regardless of who is at fault. – Gap Insurance: Useful for covering the difference between what you owe on a vehicle and its value if it’s totaled.

Car Insurance Claims

Filing a claim can be daunting, but knowing what to expect can ease the process. Document everything at the scene of an accident if possiblephotos can be invaluable. Contact your insurer as soon as you can; promptness is key to a smooth claim process.

Insider Tip: Always keep a copy of your insurance information in your vehicle. This speeds up the exchange of information in an accident.

Real-Life Example: Sarah’s Car Insurance Dilemma

Sarah, a 28-year-old marketing manager, recently purchased her first brand-new car. Excited about her new purchase, she started looking for car insurance. She was unsure about how much coverage she needed and what factors would affect her insurance rates. After doing some research, she realized the importance of understanding different coverage options and how they could benefit her in case of an accident.

Sarah’s Experience:

Sarah decided to speak with a local insurance agent to get a better understanding of her options. The agent explained the various coverage levels available and helped her determine the right amount of coverage based on her car’s value and her budget. Sarah also learned about discounts she could qualify for, such as a safe driver discount and a multi-policy discount since she already had renter’s insurance.

Thanks to the agent’s guidance, Sarah was able to secure the right coverage for her new car at an affordable rate. She felt more confident knowing she had adequate protection in place in case of any unexpected events on the road.

Car Insurance Reviews and Ratings

Before choosing an insurer, it’s wise to research their reviews and ratings. Sites like J.D. Power and Consumer Reports offer insights into customer satisfaction and claim efficiency. I chose my current insurer based largely on their top-tier customer service ratings, and it paid off when I needed help the most.

Car Insurance FAQs

Finally, addressing some common questions can further demystify car insurance: – What happens if I miss a car insurance payment? Typically, theres a grace period, but it can lead to coverage lapse if not addressed. – Can I change my coverage amount? Yes, you can adjust your coverage as needed, but consult with your insurer to understand potential impacts on your policy.

Understanding car insurance is not just about legal compliance but about making informed choices that align with your lifestyle and financial goals. Whether you’re a new driver or looking to switch policies, arming yourself with knowledge is the best strategy.